HONG KONG, Dec 22 (Reuters Breakingviews) – At its 2021 peak, the aggregate market capitalisation of cryptocurrencies was nearly $3 trillion, roughly equivalent to the economic output of Africa. A record $630 billion poured into venture capital investments that year. Now, as interest rate hikes tear into alternative assets, money going into innovation is being reallocated.

Global VC funding fell to $329 billion in the nine months to September 2022, per a report from CBInsights, down 27% year-on-year. The liquidity crunch exposed governance flaws, dumb ideas and solutions looking for problems: metaverses, non-fungible images of bored apes, flying cars. Other ideas that appeared on the cusp of commercialisation may not be. Ford Motor (F.N) disbanded its self-driving car unit in October, for example, amid doubts about how soon vehicles will learn to drive and park themselves to the satisfaction of regulators and insurers. Elsewhere the pace of advance is slowing, such as in semiconductors.

The new buzzword is “hard tech”, which contains many fields traditionally dominated by corporate labs inside industrial giants like U.S. chip equipment specialist Applied Materials (AMAT.O). Designing microscopic robots to fight disease and biochemical computers to outperform silicon chips entails higher upfront costs and longer commercialisation cycles than the consumer app plays many Silicon Valley backers are accustomed to. Over the last decade, for every VC dollar put into nanotechnology startups trying to manipulate matter at the near-atomic scale, $44 went into fintech, Preqin data shows.

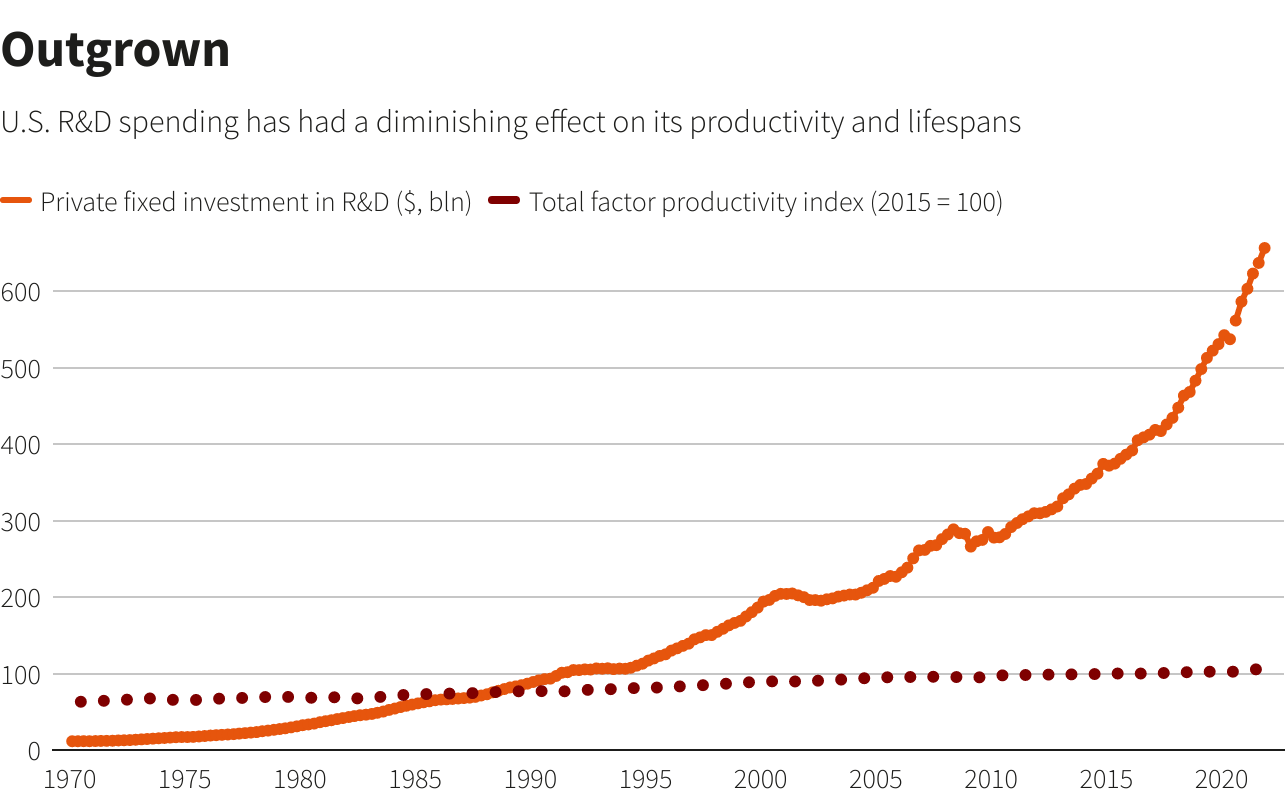

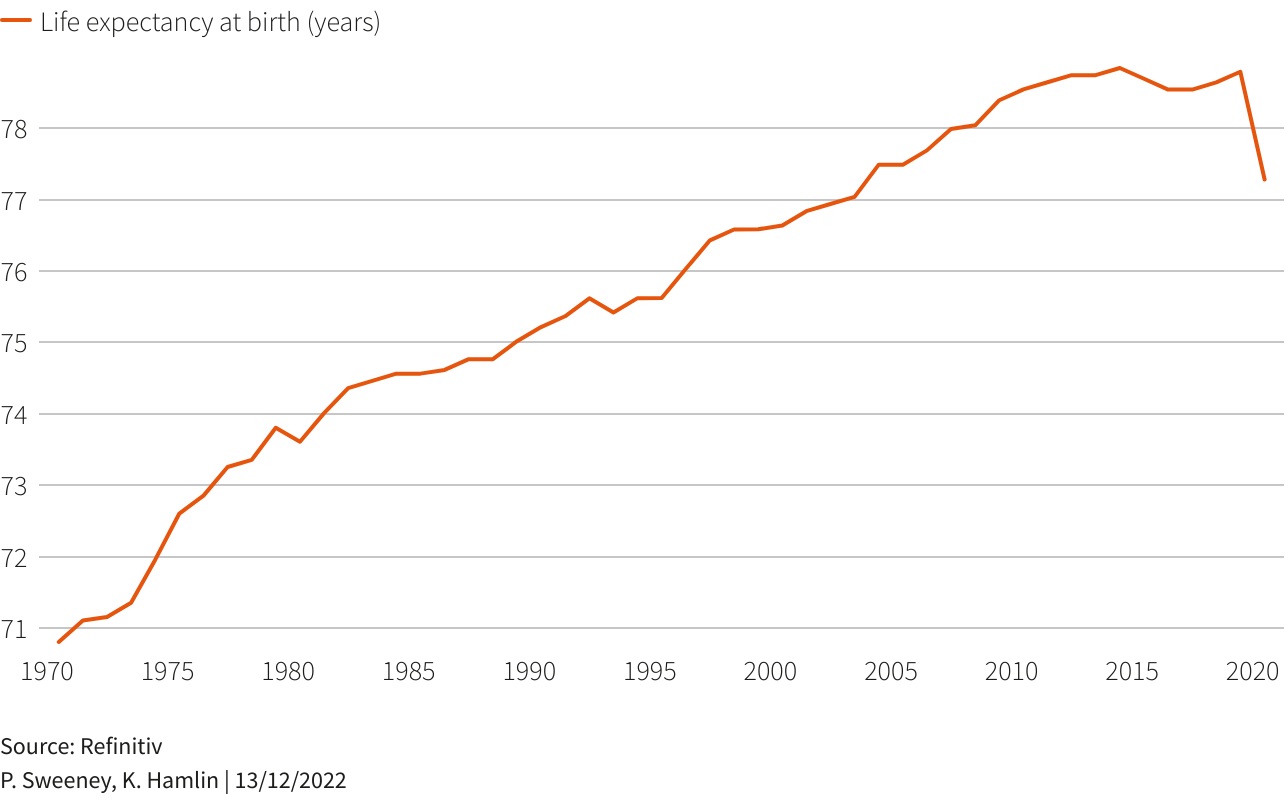

It’s high time for a shift. The exponential expansion of human output and lifespans that began with the industrial revolution in 1760 shows signs of gradually flattening out in wealthy countries, even as global patent filings continue more-or-less apace. It is striking that while U.S. research and development continue to outperform, the life expectancy of its citizens has started to decline. One factor may be the misdirection of research and the imbalanced distribution of its fruits.

At the same time, the ultra-low interest rate environment following the 2008 global financial crisis saw average quarterly VC deal values rise from below $10 billion to $178 billion at the end of 2021. Negligible yields on conventional investments encouraged staid insurers and pension plans to put money into speculative enterprises like the bankrupt crypto exchange FTX. Hopefully higher rates will push some or most of that capital back toward real problems, with big dividends for output and health. It will just take a bit longer for everyone to cash out. The enlightened capitalist will look forward to a less frivolous era.

Follow @petesweeneypro on Twitter

(This is a Breakingviews prediction for 2023. To see more of our predictions, click here.)

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias.

Asia Economics Editor Pete Sweeney joined Reuters Breakingviews in Hong Kong in September 2016. Previously he served as Reuters’ chief correspondent for China Economy and Markets, running teams in Shanghai and Beijing; before that he was editor of China Economic Review, a monthly magazine focused on providing news and analysis on the mainland economy. Sweeney came to China as a Fulbright scholar in 2008, and in that role conducted research on the Chinese aviation industry and outbound M&A. In prior incarnations he helped resettle refugees in Atlanta, covered the European Union out of Brussels, and took a poorly timed swing at craft-beer entrepreneurship in Quito even as the Ecuadorean currency collapsed (not his fault). He speaks Mandarin Chinese, at the expense of his Spanish.